Springfield Finance Director Speaks to Recent Audit and Investigation

BY JEFF SKINNER

SPRINGFIELD - On February 24, Springfield Commissioners heard an update from the city’s financial director on the recent report from the state auditors office, in which it was revealed an ongoing investigation from the state is occurring.

According to Katie Eviston, the city financial director, the city recently received the results of their audit chronicling evaluation of expenses from 2023 from the state auditors office. According to Eviston, the results did not indicate any significant issues, however she noted language in the audit report indicated that state is conducting an ongoing investigation into the city.

“I would like to clarify language that appears in the auditor of state's cover letter related to our recent audit. Under Ohio revised code, the city of Springfield undergoes an annual financial audit,” Eviston said. “Our most recent audit was completed and accepted by the auditor of state and the city received an unmodified or clean opinion, meaning our financial statements were found to be fairly presented in accordance with generally accepted accounting principles. In the auditor of state's cover letter, two sentences note that an investigation is ongoing and that results may be reported later. Transparency matters and we recognize that language like this can lead to speculation, which is why I'm speaking to this tonight. I have submitted a public records request for additional documentation from the auditor of state. While we have not yet received formal records, the auditor of state has informed us that the matter involves a complaint concerning a former employee. That is the only investigation currently underway involving the city of Springfield. There is no broader financial investigation related to the city's audit. Reviews of complaints by the auditor of state are a routine part of their oversight role and are not uncommon for public entities like Springfield. Because this is an act of review by the auditor of state, it would be inappropriate to speculate beyond what has been formally communicated. I felt it was important to address this directly so residents hear the facts clearly. We will continue to cooperate fully and share any official updates if and when they are issued by the auditor of state's office. The city's audit along with this statement will be available on the city's website tomorrow.”

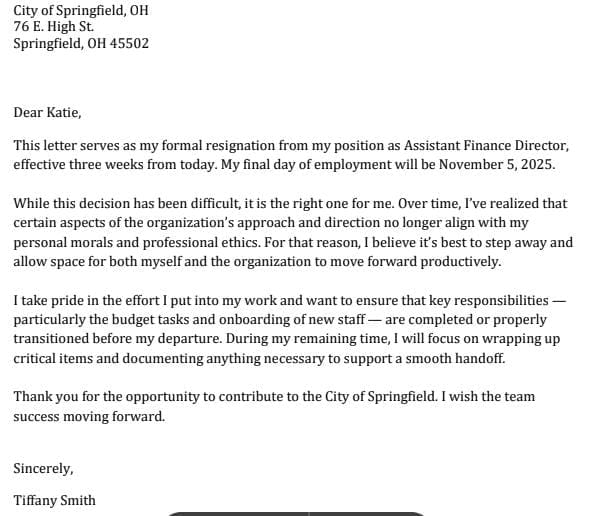

Based on Eviston’s comments, and some available information, it is possible the ongoing investigation connects with the resignation of one Tiffany Smith, whose letter of resignation indicates strong opposition to the ‘moral’ and ‘ethical’ direction of the department under Eviston.

Ironically, while many news outlets have reported the citizen complaint related to the managers airshow purchase, which led to an investigation, now a 'closed matter', the report provided by Auditor of State does not actually say that.

Alternative opinions disagree with Eviston's conclusion related to the audit from the state. Eviston argues that because the Auditor of State (AOS) looked into the complaint and chose not to issue a "Finding for Recovery" or a "Non-compliance Citation" in the final document, the expenditure was implicitly validated. In reality, Auditors "test" specific transactions based on risk or citizen tips. If the test shows the receipts exist, the travel was authorized, and the public purpose was documented, the auditor simply moves on. The absence of a "Finding" in the Schedule of Findings and Questioned Costs is what the city uses as proof of exoneration.

However, The fact the cover letter indicates there is a reference to an ongoing investigation by the Auditor of State’s Special Investigations Unit (SIU) leads critics to argue that the city cannot claim total clearance while an SIU investigation remains open. While the city is attempting to differentiate between the financial audit (which is finished and clean) and the SIU investigation (which is a separate, ongoing process), the fact they have submitted a FOIA request to the state and received no documentation in response seems to imply the argument is one of desire and not of substance.

It should be noted that a financial audit is not a forensic criminal investigation; it only looks for material errors. Provided the city has approved receipts for expenditures, it would pass a financial audit.

In addition to the aforementioned investigation, several findings were outlined in the report, including errors in financial reporting, budgetary overspending, and delayed bank reconciliations. Additionally, the report cited inadequate federal grant monitoring related to Covid-19 State and Local recovery funds.

According to the findings, the city has significant internal control deficiencies and non-compliance related to housing inspections connected to HUD program investments. Based on the report provided, Per 24 CFR §92.504(d), participating jurisdictions must monitor HOME-assisted properties to ensure compliance with HUD property standards and were not completed. Additionally, the city had multiple errors in the accuracy of the amounts reported on the quarterly Project and Expenditure Reports related to the Covid State and Local Recovery Funds. In addition, the City did not complete the required program reporting for the fourth quarter of 2022.

In response to these findings, the city reportedly promised corrective actions, such as new, stricter, financial reporting and budget oversight procedures.

Below you can find the State Auditors Report for city expenses from 2023. It does not seem to appear anywhere on the city website at this time.